Facing debt collectors in Indiana? Understanding Indiana debt collection laws protects your rights. This guide explains your protections against unfair practices and your legal options.

Key Takeaways

- Indiana’s debt collection laws are designed to protect consumers from unfair practices, mirroring federal regulations under the Fair Debt Collection Practices Act (FDCPA).

- Debt collectors in Indiana must be licensed and adhere to strict regulations, with consumers having the right to verify their legitimacy and file complaints against violations.

- Consumers have various legal recourse options against debt collectors, including the ability to sue for damages and report violations to state and federal agencies.

Overview of Indiana Debt Collection Laws

Indiana’s debt collection laws offer a robust framework designed to protect consumers from abusive and unfair debt collection practices. These laws are primarily modeled after the Fair Debt Collection Practices Act (FDCPA), which sets the standard for fair debt collection practices across the United States. Enacted in 1937, the Indiana Fair Debt Collection Practices Act complements the federal regulations, ensuring that residents are protected from harassment and unfair practices by debt collectors.

Indiana state law requires all debt collection agencies to adhere to these standards, prohibiting harassment, threats, and deceptive practices. This dual layer of protection—state or federal court and state—provides Indiana residents with a comprehensive shield against unfair debt collection tactics.

Understanding these consumer law enables you to protect your rights and confidently confront debt collectors owing to your hearing knowledge.

Federal Protections for Indiana Residents

Federal law, particularly the Fair Debt Collection Practices Act (FDCPA), plays a crucial role in protecting Indiana residents from abusive debt collection practices. Enforced by the U.S. Federal Trade Commission (FTC), the FDCPA sets the standard for how debt collectors must conduct themselves when attempting to collect debts. This law covers personal, family, and household debts, ensuring that consumers are treated fairly and respectfully.

A key element of the FDCPA is that it permits consumers to assert their claims if they feel harassed or treated unfairly by debt collectors. For instance, consumers can request a written document validating their debts within five days of initial contact, ensuring that they have accurate information.

Additionally, violations of the FDCPA can be reported to the (CFPB), which oversees the enforcement of consumer protection laws and ensures that debt collectors comply with federal regulations.

Licensing Requirements for Debt Collectors in Indiana

In Indiana, debt collection agencies must be licensed to operate legally, ensuring that they adhere to fair debt collection practices. The Indiana Secretary of State is responsible for issuing these licenses, and debt collection agencies must register through the Nationwide Multistate Licensing System (NMLS). This process includes providing detailed information such as the name, residence address, office business address, and qualifications of the individuals applying for the license.

A bond may also be required as part of the licensing process, adding an extra layer of security for consumers with the intention of protecting their interests. The license is valid for two years, after which it must be renewed to ensure continuous compliance with Indiana state law.

Requiring debt collectors to be licensed enhances consumer protection and protects consumers in Indiana, ensuring that only qualified entities can collect debts.

How To Verify a Debt Collector’s License

Verifying a debt collector’s license is crucial for protecting yourself from potential scams and illegal practices. Consumers can verify a debt collector’s license by:

- Visiting the Indiana Secretary of State’s website

- Checking the status and validity of the license

- Reviewing any disciplinary actions against the debt collector

- Ensuring the debt collector operates within the legal framework set by Indiana law

Taking the time to verify a debt collector’s license ensures that the collection agency is legitimate and compliant with fair debt collection practices. This simple step can save you from falling victim to fraudulent activities and reinforces your confidence in dealing with debt collectors.

Consumer Rights Under Indiana Law

Indiana law provides consumers with specific rights designed to protect them from unfair debt collection practices. These rights are in addition to those provided by the federal Fair Debt Collection Practices Act (FDCPA), ensuring a broader spectrum of protection for Indiana residents. Knowing your rights under Indiana state law enables you to effectively confront debt collectors and prevent any illegal practices.

Knowing these rights is crucial for anyone dealing with consumer debt, empowering you to take appropriate action if a debt collector oversteps their bounds. From the moment a debt collector contacts you, being aware of your rights and the protections under the law is crucial.

Prohibited Practices by Debt Collectors

Debt collectors in Indiana are prohibited from engaging in the following abusive and unfair practices:

- Harassment, such as threats of violence or abuse

- Use of obscene or profane language

- Providing inaccurate information or using false representations to mislead consumers

- Engaging in deceptive practices and making material false statements, which are classified as unfair and illegal under Indiana law, including harassment debt collectors and the unfairness debt collectors.

Violating these prohibitions can lead to serious consequences for debt collectors. For example, a violation of the Indiana Fair Debt Collection Practices Act is classified as a Class B misdemeanor, highlighting the state’s commitment to protecting consumers from unfair treatment, violating consumer protection laws.

Debt collectors are also not allowed to disclose information about a debt to anyone other than the consumer or their attorney, ensuring privacy and confidentiality.

Legal Actions Consumers Can Take

If a debt collector violates your rights under Indiana law, there are several legal actions you can take. Consumers have the right to request licensing information from a debt collection agency to verify its legitimacy. Additionally, violations of the Indiana Fair Debt Collection Practices Act can be prosecuted by the prosecuting attorney of any judicial circuit.

Consumers can also dispute a debt at any time and request a debt validation letter within five days of initial contact. If a debt collector reports incorrect information about your credit report, you can sue them under the Fair Credit Reporting Act and potentially recover damages for emotional stress, statutory damages, court costs, and attorney’s fees.

The potential outcomes of suing a debt collector for FDCPA violations include actual damages plus up to $1,000 in statutory damages.

Statute of Limitations on Debt Collection in Indiana

The statute of limitations on debt collection in Indiana varies depending on the type of debt:

- For most consumer debts, including mortgage, medical, and credit card debts, the statute of limitations is six years.

- Car loan debts have a statute of limitations of four years.

- State tax debts carry a statute of limitations of ten years.

Knowing the statute of limitations is crucial for consumers, as it determines how long a creditor has to initiate legal action for debt collection. The time limit begins from the date of the last activity on the account, so it’s important to keep track of this date to protect yourself from potential legal actions after the statute of limitations has expired.

Legal Recourse Against Debt Collectors

If you believe your rights have been violated by a debt collector, there are several steps you can take to seek legal recourse. Consumers can file a complaint with the appropriate state or federal agencies to report the violation. Additionally, consumers have the option to sue the collection agency for violations of their rights, which can result in the recovery of damages.

Taking legal action against a debt collector can be a powerful way to hold them accountable for their actions. It also serves as a deterrent against future violations, ensuring that debt collectors adhere to fair debt collection practices and respect consumer rights.

Filing Complaints With State and Federal Agencies

Filing a complaint with state and federal agencies is a crucial step in reporting debt collection violations. In Indiana, consumers can report issues with debt collectors to the Indiana Secretary of State. Additionally, complaints can be submitted online to the (CFPB), which oversees the enforcement of consumer protection laws.

Before filing a complaint, consumers should compile supporting documents for their claim, such as copies of letters, emails, and any other correspondence with the debt collector. Reporting violations to the Indiana Attorney General is another option for enforcement and can help ensure that debt collectors are held accountable for their actions.

Suing for FDCPA Violations

Suing for violations of the Fair Debt Collection Practices Act (FDCPA) can provide consumers with a powerful means of redress. If a debt collector violates the FDCPA, consumers can:

- Sue for damages of up to $1,000

- Recover statutory damages

- Recover court costs

- Recover attorney’s fees

However, it’s important to notice that lawsuits must be filed within one year of the violation.

Consulting with an attorney before filing a lawsuit is highly recommended; they can provide guidance and ensure your case is presented effectively. Legal action allows consumers to hold debt collectors accountable and potentially recover damages for the harm caused by their violations.

What Debt Collectors Are Allowed To Do

While debt collectors are subject to strict regulations, they do have certain legal rights when it comes to collecting debts. In Indiana, debt collectors can initiate lawsuits to obtain judgments for unpaid debts, which can lead to wage garnishment or property liens. They also have the authority to seize property, including vehicles, without needing a court order.

Knowing what debt collectors are legally allowed to do helps consumers navigate the debt collection process more effectively. It also highlights the importance of knowing your rights to ensure that debt collectors do not overstep their legal boundaries.

Wage Garnishment Procedures

In Indiana, wage garnishment is a common outcome if debtors fail to respond to a court summons. Debtors must respond within 20 days if the summons is delivered personally, or within 23 days if it is mailed.

If they fail to appear in court, the judge may order wages garnishment to repay the unpaid debt, and they could happen to be sued for judgment.

Repossession Rules

Repossession rules in Indiana allow lenders to repossess a vehicle if the borrower defaults on their auto loan, even after a single missed payment. This process does not require prior court approval, making it crucial for borrowers to stay current on their payments.

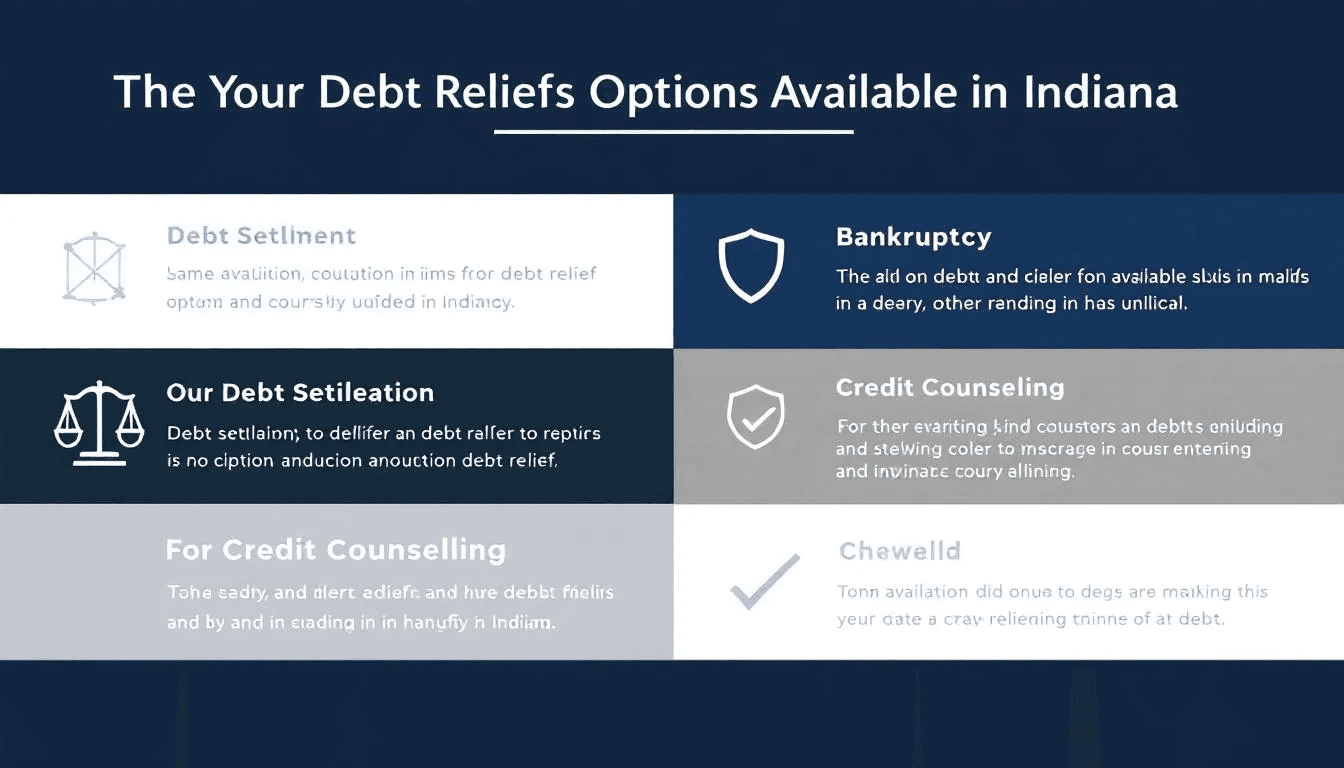

Options for Debt Relief in Indiana

Indiana residents have several options for debt relief, each offering different advantages and considerations. Debt management involves working with an agency to negotiate better repayment terms with creditors, allowing consumers to make one monthly payment while paying off their money debt.

Debt consolidation combines multiple debts into a single loan, often with a lower interest rate, simplifying the repayment process. Debt settlement allows consumers to negotiate with creditors to pay less than the total debt owed, typically in a lump sum.

For those in severe financial distress, bankruptcy is a legal process that can eliminate or restructure debts, providing a fresh start. Each of these options has its pros and cons, and it’s important for consumers to carefully consider their situation and seek professional advice if needed.

Summary

Navigating the world of debt collection can be challenging, but understanding the laws and protections available to you can make a significant difference. Indiana’s debt collection laws, combined with federal protections, provide a comprehensive framework to protect consumers from abusive and unfair practices. Knowing your rights and the steps you can take if they are violated empowers you to handle debt collectors with confidence.

Whether you’re dealing with debt collectors, considering legal action, or exploring debt relief options, this guide provides the essential information you need. By staying informed and proactive, you can navigate the complexities of debt collection and take control of your financial future.

Frequently Asked Questions

Are you legally obligated to pay collections?

You are legally obligated to pay collections if the debt is legitimate. However, you have the right to direct how payments are applied to your debts.

How can I verify if a debt collector is licensed in Indiana?

To verify if a debt collector is licensed in Indiana, visit the Indiana Secretary of State’s website to check the status and validity of their license. This ensures you are dealing with a legitimate collector.

What should I do if a debt collector harasses me?

If a debt collector harasses you, it is essential to file a complaint with state or federal agencies and explore legal action for any violations of your rights. Taking these steps can help protect you from further harassment.

What is the statute of limitations for credit card debt in Indiana?

The statute of limitations for credit card debt in Indiana is six years from the date of the last activity on the account. Therefore, it is crucial to be aware of this timeframe when managing such debts.

Can debt collectors garnish my wages in Indiana?

Yes, debt collectors can garnish your wages in Indiana if they secure a court judgment against you and you do not respond to the court summons.